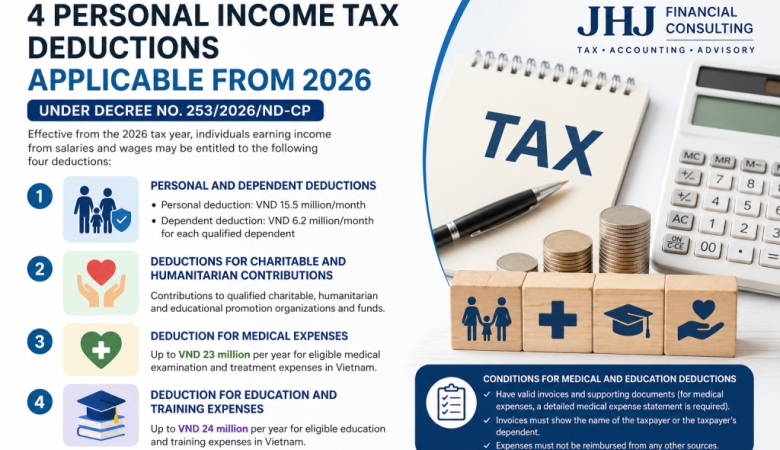

Four Personal Income Tax Deductions Applicable from 2026 under Decree No. 253/2026/ND-CP

To reduce the tax burden on employees, the Vietnamese Government has introduced several changes to the Personal Income Tax (PIT) deduction regime under Decree No. 253/2026/ND-CP. Effective from the 2026 tax year, individuals earning income from salaries and wages may be entitled to four types of tax deductions, provided that they satisfy the prescribed conditions.

1. Personal and Dependent Deductions

The standard family circumstance deduction includes:

- Personal deduction: VND 15.5 million per month (VND 186 million per year).

- Dependent deduction: VND 6.2 million per month for each qualified dependent (VND 74.4 million per year).

Taxpayers must register their dependents and provide supporting documentation in accordance with Vietnam's tax regulations.

2. Deductions for Charitable and Humanitarian Contributions

Taxpayers may deduct eligible contributions made to qualified charitable and humanitarian organizations, including:

- Organizations and institutions providing care for disadvantaged children, persons with disabilities, and elderly individuals without support;

- Charity funds, humanitarian funds, and educational promotion funds;

- Organizations legally established to mobilize charitable donations.

The receiving organizations or funds must be duly established or officially recognized by competent state authorities and operate exclusively for charitable, humanitarian, or educational purposes on a non-profit basis.

To qualify for the deduction, taxpayers must retain valid supporting documents, such as official donation receipts or proof of non-cash payment through a licensed financial institution.

3. Deduction for Medical Expenses

Beginning in 2026, taxpayers may claim a deduction of up to VND 23 million per year for eligible medical expenses incurred at healthcare facilities in Vietnam.

The deductible expenses are limited to medical examination and treatment costs that fall within the list of services covered by Vietnam's Health Insurance scheme.

4. Deduction for Education and Training Expenses

Taxpayers may also claim a deduction of up to VND 24 million per year for eligible education and training expenses incurred at educational institutions in Vietnam.

Eligible expenses include:

- Preschool tuition;

- Primary and secondary education tuition;

- Vocational education tuition;

- University tuition;

- Tuition fees for professional skills and specialized training programs provided by legally established educational institutions.

This new deduction is intended to encourage investment in education and professional development.

Conditions for Claiming Medical and Education Deductions

Medical and education expenses are deductible only if all of the following conditions are satisfied:

- Valid invoices and supporting documents are available. For medical expenses, taxpayers must also obtain a detailed medical expense statement issued in accordance with regulations of the Ministry of Health.

- The invoices or supporting documents must clearly identify either the taxpayer or the taxpayer's qualified dependent.

- The expenses must not have been reimbursed or compensated from any other source, including government funding, sponsorships, employer reimbursement, social insurance, health insurance, or any other insurance program.

Legal Basis

The above deductions are stipulated in Article 49 of Decree No. 253/2026/ND-CP and apply to Personal Income Tax calculations from the 2026 tax year onward.