REQUIRED TO FILE PIT RETURNS ON A QUARTERLY BASIS ONLY FROM Q2 2026

Monthly Personal Income Tax (PIT) Filing Suspended under Resolution No. 66.16/2026/NQ-CP

To simplify tax compliance procedures and reduce administrative burdens for businesses, the Government has issued Resolution No. 66.16/2026/NQ-CP, which temporarily suspends the requirement for monthly Personal Income Tax (PIT) declarations.

Accordingly, during the period from 15 April 2026 to 28 February 2027, enterprises are only required to submit PIT returns on a quarterly basis and are no longer required to file monthly PIT returns.

This measure is expected to reduce the number of tax filings throughout the year, thereby saving time and compliance costs for taxpayers.

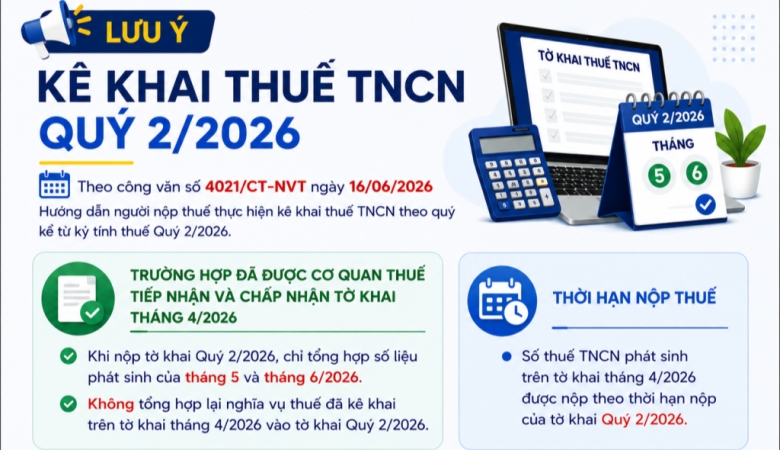

Transitional Guidance for Q2 2026 PIT Filing

On 16 June 2026, the tax authority issued Official Letter No. 4021/CT-NVT providing guidance on the implementation of quarterly PIT filing starting from the tax period of Q2 2026.

According to the Official Letter, taxpayers who have already submitted their PIT return for April 2026 and received acceptance confirmation from the tax authority should note the following:

1. Include Only May and June 2026 Data in the Q2 2026 PIT Return

When preparing the PIT return for Q2 2026, taxpayers should only report PIT liabilities arising in May and June 2026.

Tax liabilities that have already been declared in the April 2026 PIT return must not be included again in the Q2 2026 PIT return in order to avoid duplicate reporting.

2. Extended Payment Deadline for PIT Declared in April 2026

PIT liabilities reported in the April 2026 PIT return may be paid by the payment deadline applicable to the Q2 2026 PIT return.

This transitional arrangement helps businesses better manage cash flow and facilitates the shift from monthly to quarterly PIT filing.

Key Considerations for Enterprises

To ensure compliance and avoid filing errors, enterprises should:

- Review the April 2026 PIT return that has already been accepted by the tax authority;

- Include only PIT liabilities arising in May and June 2026 in the Q2 2026 PIT return;

- Avoid duplicating figures already declared for April 2026;

- Monitor the filing and payment deadlines applicable to Q2 2026.

Timely understanding and proper implementation of these transitional provisions will help enterprises minimize compliance risks and avoid unnecessary amendments or administrative penalties.