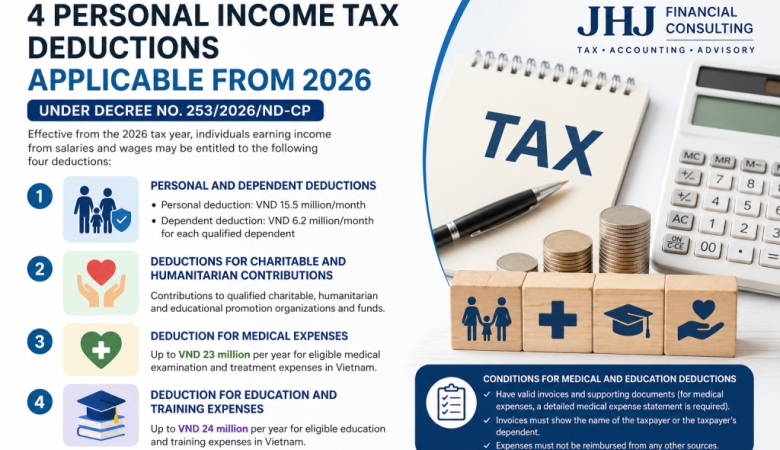

BUSINESS HOUSEHOLDS TAX FROM 2026

Personal Income Tax Law 2025 No. 109/2025/QH15, Value Added Tax Amendment Law No. 149/2025/QH15.

Accordingly, from 2026, the tax authorities will completely terminate the presumptive tax collection mechanism and shift to the self-declaration and self-payment mechanism as prescribed by the Law on Tax Administration.

Specifically, according to Article 7 of the Personal Income Tax Law and Decision No. 3389/QD-BTC, business households will be classified into three new groups for tax administration as follows:

Group 1: Annual revenue below VND 500 million

- Exempted from value-added tax (VAT) and personal income tax (PIT).

- Not required to apply complicated accounting books but must still make periodic declarations.

- May choose to declare twice a year (at the beginning and in the middle or at the end of the year) or at other suitable times.

Group 2: Annual revenue from VND 500 million to below VND 3 billion

You can choose one of the following two methods for calculating tax:

1. Calculate tax directly on revenue exceeding the limits specified in GROUP 1.

- Tax rates by business line:

- 1%: Distribution and supply of goods

- 3%: Production, transportation, services associated with goods, and construction with material supply

- 5%: Services and construction without material supply

- 2%: Other business activities

- Required to make declarations four times a year (quarterly).

- Business households with annual revenue exceeding VND 1 billion in the retail or consumer service sector must issue e-invoices from cash registers connected to the tax authority.

- Those with annual revenue below VND 1 billion are not required but encouraged to record their revenues fully.

2. Calculating tax on taxable income

Personal income tax on business income of resident individuals is determined by multiplying taxable income by the tax rate. Where:

- Taxable income is determined by the revenue from the sale of goods and services minus (-) expenses related to production and business activities during the tax period.

- Tax rate of 15%.

Group 3: Annual revenue exceeding VND 3 billion

- Business households with annual revenue exceeding VND 3 billion for two consecutive years shall be classified into this group.

- Apply the credit method for VAT calculation:

VAT payable = Output VAT – Input VAT

- PIT calculated at 17% on total profits, in which:

Profit = Revenue – Deductible expenses

- Households with annual revenue exceeding VND 50 billion shall make monthly tax declarations; those with revenue below VND 50 billion shall declare quarterly.

- Required to issue e-invoices and open a separate bank account for business transactions.

- The use of e-invoices with tax codes or e-invoices generated from cash registers is mandatory

SUMMARY TABLE OF PERSONAL INCOME TAX RATES FROM BUSINESS ACTIVITIES IN 2026

Case | Personal income tax rate 2026 (%) | Personal Income Tax Calculation Formula 2026 | |

Determine the cost | Revenue from 500 million to under 3 billion | 15% | (Revenue – Expenses) x 15% |

| Revenue ranges from 3 to 50 billion. | 17% | (Revenue – Expenses) x 17% | |

| Revenue exceeding 50 billion. | 20% | (Revenue – Expenses) x 20% | |

| Costs are not determined (This only applies to revenue groups under 3 billion.) | Distribution and supply of goods | 0.5% | (Revenue – 500 million) x 0.5% |

| Production, transportation, services related to goods, and construction with material procurement included. | 1.5% | (Revenue – 500 million) x 1.5% | |

| Services and construction without material procurement. | 2% | (Revenue – 500 million) x 2% | |

| Providing digital content products and services related to entertainment, video games, digital movies, digital photos, digital music, and digital advertising. | 5% | (Revenue – 500 million) x 5% | |

| The remaining sectors | 1% | (Revenue – 500 million) x 1% | |